- Refining VC

- Posts

- Founders Don't Care About Thought Leadership

Founders Don't Care About Thought Leadership

The VC marketing mistake that makes funds invisible to founders — and how outside-in content fixes it.

Laurie Owen

March 19, 2026

A founder is looking to raise. They open ChatGPT and type - “who are the best biotech funds investing at inception stage in Europe?” They get an answer. Four funds, named with confidence, delivered with the authority of definitive fact.

Your fund isn't one of them.

Not because you're not good enough. Because the algorithm has no evidence that you're the right answer to that question.

There's the old adage that nobody cares about you - they care about what you can do for them. It's a bit sad, a bit transactional, but entirely true inside business hours.

A founder fundraising is unlikely to read your thesis on the Future of Deep Tech because they find it intellectually stimulating. They're asking the question, how is this relevant to me. If your content doesn’t answer that, you might invisible at the exact moment it matters most.

Most VC content is ‘inside-out’. The best content is ‘outside-in’.

The difference has always mattered… but with LLMs in the mix, it's starting to matter a lot more…

Founders have two modes

Strip it back and founders are doing one of two things at any given moment.

1) They are looking for funding.

2) They are trying to operate.

In practice, looking for funding means they are building a list, doing due diligence on potential investors, trying to understand who the right people are for their specific stage and sector.

They are asking discovery questions. Who backs companies like mine? Who has conviction in this space? Who do other founders say is good to work with?

This is the moment where your brand, reputation, and ‘find-ability’ converge.

In practice, trying to operate means they are problem solving. They have a hiring problem, a pricing problem, a co-founder conflict, a board they do not know how to manage. They are not looking for a fund to back them - they are looking for a specific answer to a specific problem (usually urgently) and probably without the bandwidth to engage with content that doesn't directly address their issue.

Every piece of content a VC produces is either useful at one of those two moments, or it is content for other VCs and LPs. Which, to be clear, is a legitimate content goal.

But it is worth being honest about who you are writing for, because funds can believe they are “producing content for founders” and are producing content that founders never read.

In defence of thought leadership (and its limits)

Writing is thinking. This is one of the genuine and underappreciated functions of content in venture. The act of publishing a thesis or POV - forces a clarity of thought.

Some of the best VC writing exists because the partner writing process sharpened their conviction. We can call this is inside-out thinking.

Alfred Lin published a piece this week on market sizing that went broadly viral within the ecosystem. It is sharp and useful to anyone trying to think about markets (VCs).

It is the kind of content that builds a personal brand and earns respect from LPs, other investors, and the broader tech community. None of that is trivial.

But it is primarily interesting to people who are already thinking about markets in the abstract - a founder reading it is probably doing so because they follow Alfred Lin personally, less so because they searched for it at a moment of need.

As a massive venture content nerd, when I think about the “iconic pieces” that have actually lasted - almost all of them are founder-facing.

Even Naval, built his reputation before the philosophical profile and before AngelList, co-authoring a guide specifically to teach entrepreneurs how to raise venture capital.

All were almost universally written for the person on the other side of the table, not for the investor's peers.

That is not a coincidence. The VC writing that lasts is outside-in.

Before you plan content, think - is a founder searching for this? Or are you just saying something you want to say?

See, Pick, Win

From the VC side, those are the three jobs. Everything else is in service of one of them.

Outside-in content maps directly onto See, Pick, Win because it works at both moments, discovery (funding) and problem solving (operating). Inside-out content instead speaks to people who are already paying attention, not to founders who are searching for something.

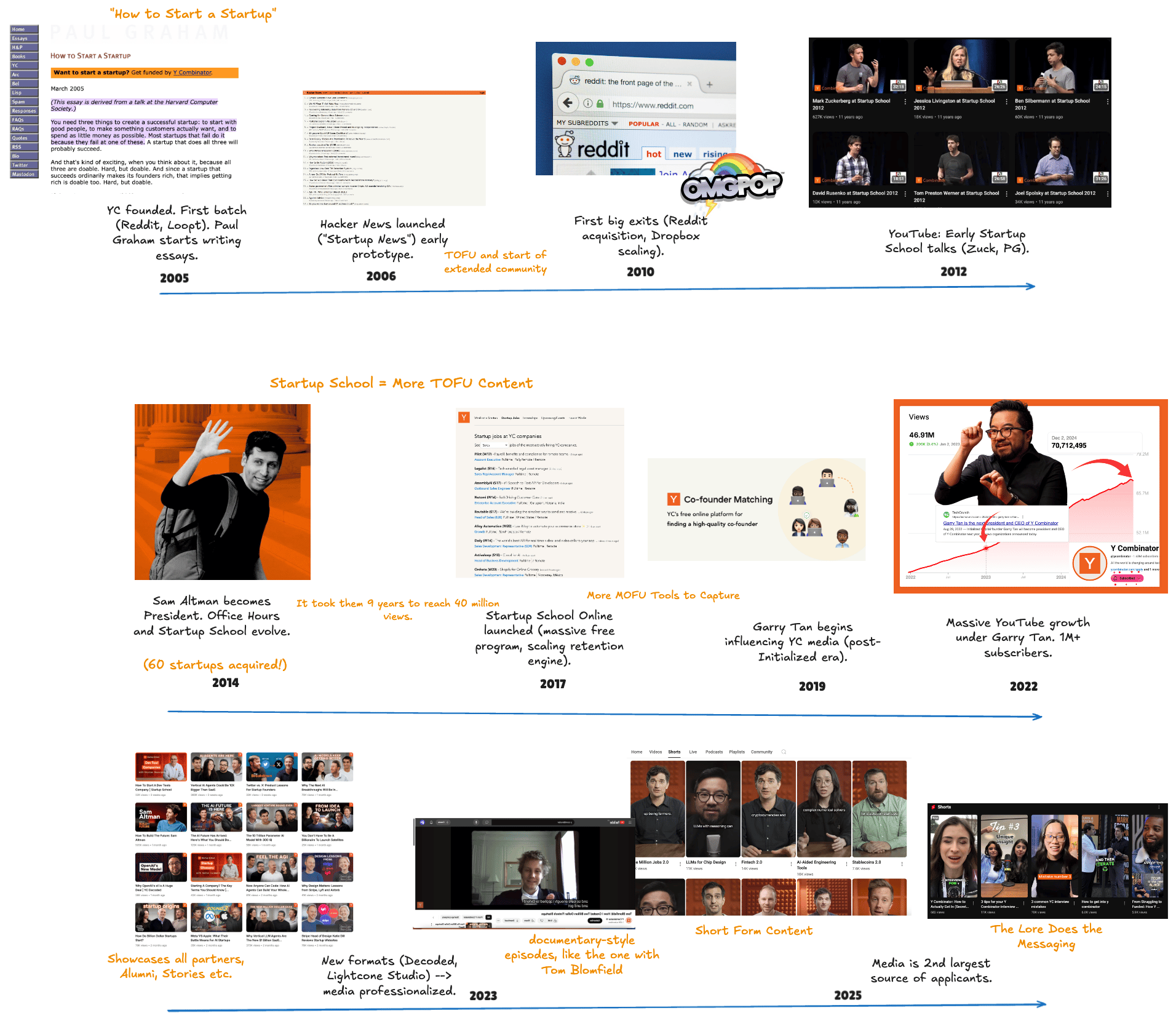

YC has spent fifteen years doing all three, at scale, better than anyone else in the industry (much more on that here).

Startup School, PG essays, the podcast, hackernews, the alumni network - all of it maps directly onto what early-stage founders are trying to figure out at the moment they need it.

The vocabulary, the frameworks, the mental models - default alive, ramen profitable, do things that don't scale - these are industry constructs that founders now use without realising where they came from.

That is not brand marketing. That is 15 years of outside-in content compounding into an almost insurmountable advantage across See, Pick, and Win simultaneously.

YC sees more deals because founders find them earlier and trust them before the first meeting. Founders pick YC because the relationship is already built by the time they are raising. YC wins allocation because by the time a round is happening, YC is the default option.

The challenge for everyone else

The complication in this specific example is that YC's methodology is not universal, and for funds operating in very different contexts, YC filling the vacuum by default is not a positive outcome (!).

Take a fund investing at inception stage in highly specific verticals, or perhaps looking to back researchers/operators approaching company-building from a different starting point (or age)…

… The questions those individuals are asking are v different. They might be asking about clinical trial design, regulatory strategy, patents, or how to think about specific commercialisation timelines.

If that fund is not producing content that serves those founders at their specific moment of need, YC content fills the gap by default. Not because YC is trying to… but because YC's content is everywhere and theirs is not.

Founders can show up pre-loaded with frameworks optimised for a path that looks nothing like the one their sector investors want them to walk.

The outside-in content gap can go beyond just a marketing problem, and become a self-inflicted portfolio problem.

Why this is about to matter more

This has always been the underlying issue with VC content. But it was tolerable when the cost of being unfindable was just lower organic traffic, and when Google at least served up ten results and let the user infer and triangulate across them.

The LLM shift removes that tolerance entirely.

When the founder types "who are the best X funds" they do not get a list of links to evaluate, there is no page two, there is no "also consider."

If your fund is not in it, you do not exist for that founder at that moment.

None of your worthwhile activity matters if the an LLM does not have enough signal to surface you for the right query.

The funds that will be in that answer are the ones that have spent years producing content that is genuinely useful to the people searching for it (this is testable and provable).

Content that is actually good for the person who needs it - it turns out, is also what algorithms will reward.

Funds that figure out the outside-in shift first will have built a compounding advantage before most of their competitors have noticed the problem. Which is, of course, exactly how every durable advantage in venture gets built.

Laurie, Refinery Media

If you made it all the way through, thanks so much for reading! Several hundred VCs now open this every week. If it's helped you think differently about marketing, Venture, or storytelling, please send it to someone in your orbit.

If you enjoyed this, read more from our top posts: