- Refining VC

- Posts

- The Marketing Inflection Point

The Marketing Inflection Point

Why the emerging vs established distinction is the wrong frame - and what to use instead

Laurie Owen

April 09, 2026

This week I published a 6000 word piece for Murph Capital on how Emerging Managers should approach Marketing.

There was a lot to cover, and as always I tried to supply sufficient examples for each concept. If you work at or advise an early stage fund, it's worth reading in full. Here.

The TLDR is… “Emerging” Managers have a set of structural advantages in content that established funds have lost and cannot easily get back -

Specificity

Transparency

Proximity to community

Funds breaking through are not the ones producing more content, but the ones making their work most visible. Their process, their thesis in formation, their real proximity to founders. Not a performance of all that. The thing itself.

So what about bigger funds?

This newsletter takes the same ideas and asks what they mean across the full spectrum - because the marketing lessons do not stop being relevant when a fund matures - but the job changes.

A New Way to Categorise Funds

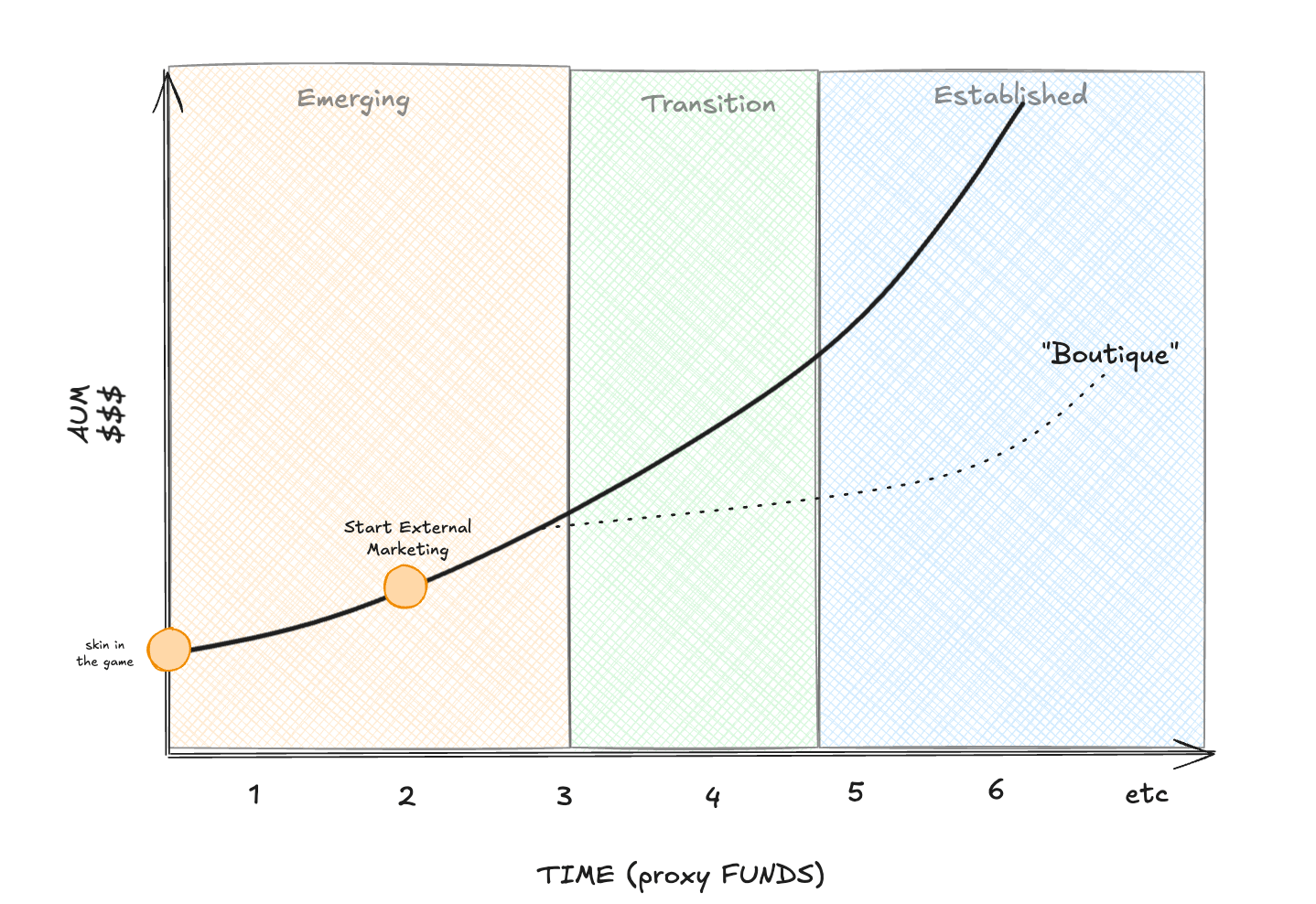

The industry uses "emerging manager" as a fundraising category.

Sub $100M, Fund I-III, still building the track record. It is a useful shorthand for where you are in the capital stack. But from a marketing perspective, it is fairly unhelpful:

It draws a binary distinction between emerging and established funds as something related to time. This is why we see a lot of newer managers or funds only begin marketing around Year 3 or Fund II.

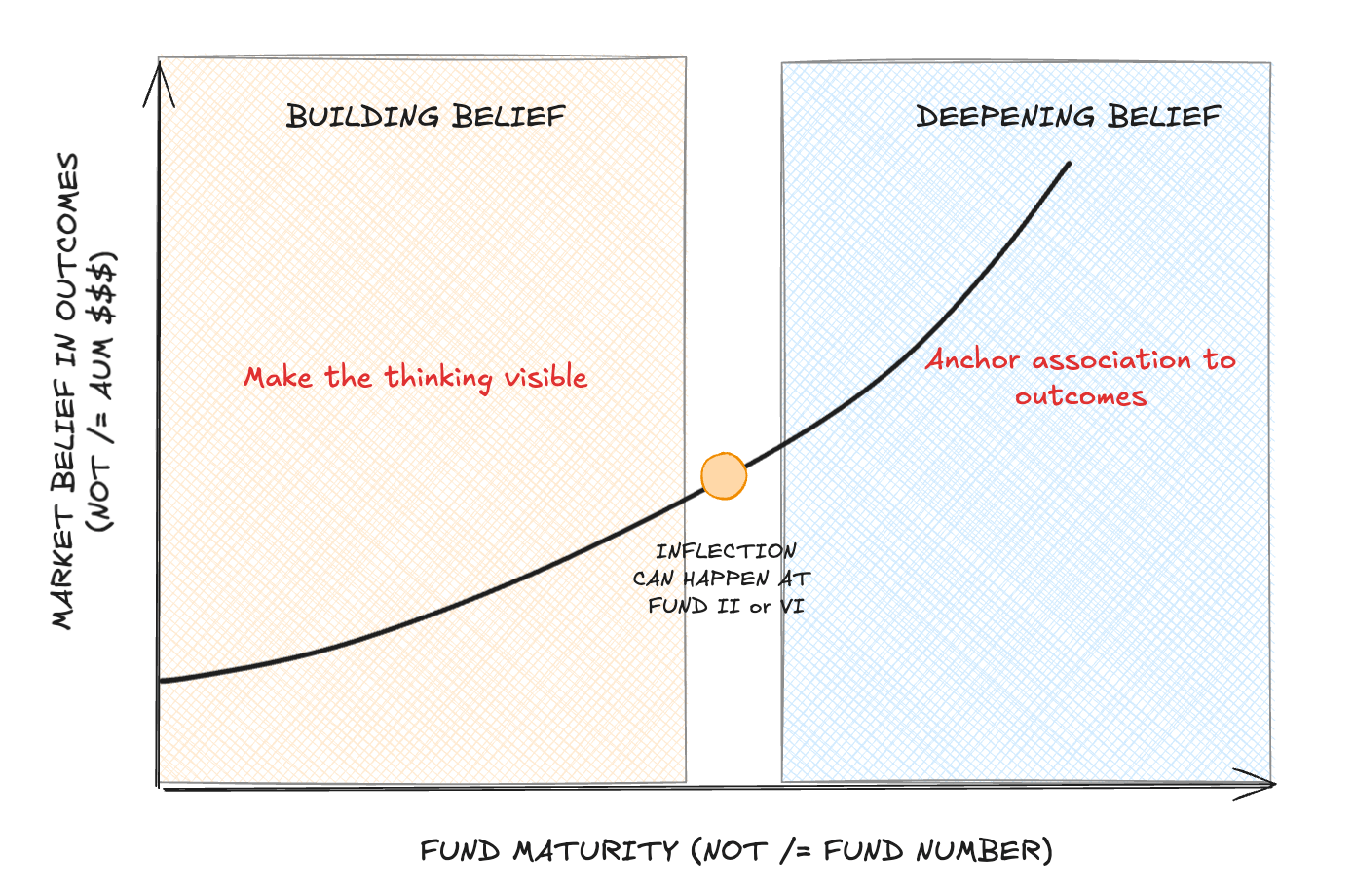

It is much more useful to assume marketing is needed, and draw a line instead between funds that have public outcomes and funds that do not.

The Murph Capital piece goes in depth about before you cross that inflection.

But after crossing that, the centre of gravity shifts. Outcomes become the proof and the thinking becomes the context that makes those outcomes legible.

Before outcomes → signal = proximity, process, taste

After outcomes → signal = association, narrative, compounding

Broadly, the mistake funds make is misreading which side of that line they are on… and producing the wrong kind of content as a result.

Pre-inflection funds try to look post-inflection - polished, outcome-focused, when they have no outcomes yet. The effect is a kind of hollow authority or content that lands as performance because the market has no prior to attach it to.

Post-inflection funds stay stuck in broadcast mode - announcing wins without ever showing the work that produced them. Which is a waste, because at that stage they have the most interesting material available and the credibility to make it land.

Both are leaving the most valuable thing on the table.

The thread that runs through both

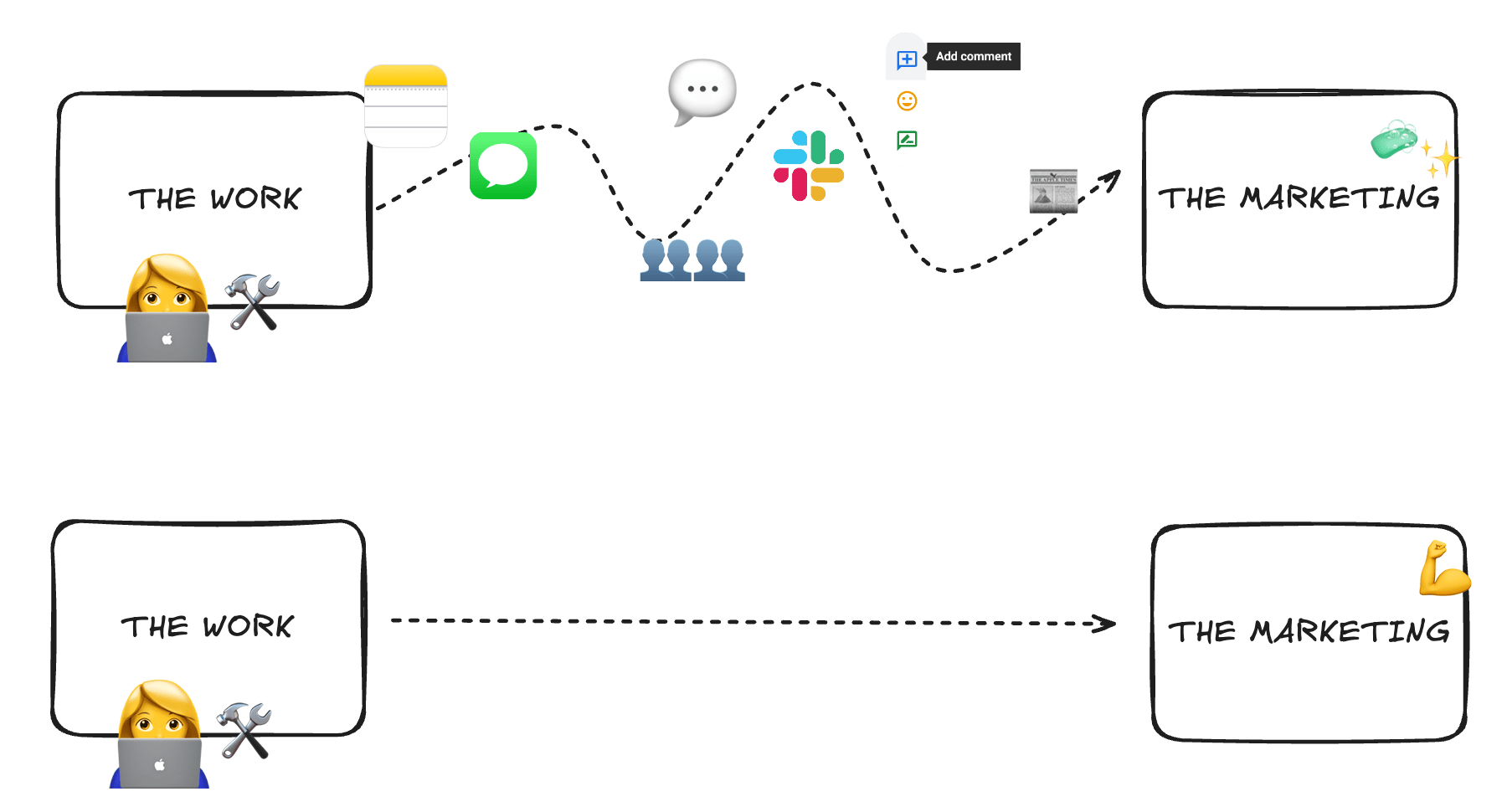

The connective tissue, at every stage, is making the doing visible.

This is the thing most funds miss regardless of where they are in the lifecycle. Comms and PR sit in a box. Everything gets sanitised. The gap between the work and the communication is so wide, and so filtered, that by the time it reaches the public the texture is gone.

Before the inflection, the doing is boots on the ground. Founder proximity, community, data from the process.

This signals in two directions simultaneously: to founders, that you understand their world; to LPs, that you can see, pick, and win. That dual signal compounds. The Murph piece covers this in detail - the specificity advantage, the transparency advantage, what it looks like to build a frame from scratch.

After the inflection, the doing looks different. LPs investing in an established fund already assume you can see, pick, and win - that is why they are there. What they are now evaluating is whether the outcomes compound.

This is also why mega funds are increasingly under pressure - the multiple coming back to LPs is compressing even as the guarantee of some return goes up. The job of content shifts accordingly.

At this stage, the work itself - the portfolio stories, the thesis plays, the platform work, the company moments - should be producing the body of content that markets the fund.

The association between a fund and its winners is not automatic. It has to be built deliberately, and many funds are not associated strongly with their winners.

I have written about this before because it is one of the most persistent gaps I see across the market.

The process is the problem

The irony is that as funds scale, they add infrastructure that makes this harder rather than easier. PR reviews, communications checks, brand approvals, legal sign-off.

Some is necessary but a lot of it just widens the gap between the work and the communication.

The best established funds have figured out a version of this that still works at scale. The content is anchored to something real.

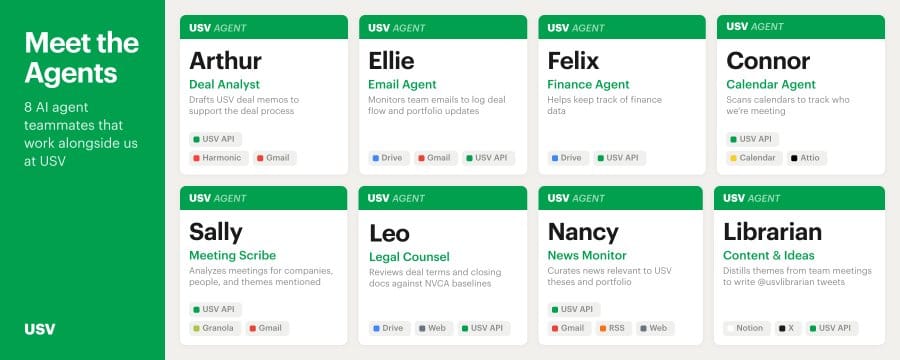

I think a stellar example of this is USV.

The core point is that USV's best content - both historically and recently - works because it's rooted in what they're actually doing, rather than anything performative.

Fred Wilson's early blog wasn't him positioning himself as a thought leader handing down wisdom. It was just him writing about his day-to-day work with founders - answering their questions, sharing what he was doing. Even his more theoretical but hugely popular MBA Mondays was skewed this way - it felt real because it was real.

USV’s recent AI agents piece follows the same logic. Instead of writing "here's our thesis on AI agents" - which any firm could do - USV wrote here's how we are literally using AI agents inside our firm right now.

That specificity and transparency is what makes it 10x more interesting. It's evidence, not opinion.

The broader point is that firms think they need to “marketing” to be credible, when actually the most compelling content is just a honest account of the work itself.

Similarly, the most powerful brand asset a post-inflection fund has is its winners, and association with them - we can look at classic examples of funds showing the work.

a16z and Flock Safety

a16z has threaded it through a broader narrative about public safety infrastructure, and in content have used Flock - featuring their policy team and government network to show how a16z operates at municipal and federal level, not just at the company level.

Flock's founder has appeared on a16z podcasts about building safer communities, about eliminating crime, about real-world technology. Less specifically about Flock, but a16z’s views on each.

NFX and Lyft

NFX's entire content operation is built around the theory of network effects and marketplace businesses - and Lyft is the example they return to constantly, across their own content and in external PR and podcast appearances.

The pattern works once you see it. YC retelling the Airbnb cereal box story frequently, or the story of Stripe manually adding themselves to Hackernews Devs projects, or even Sequoia's Don Valentine original note on Apple circulating this week - doing more brand work than most content operations do in a year.

But the gap between what funds could be doing here and what most are doing remains significant.

NEO is a timely example of that gap... They have Cursor and Kalshi, and NEO has impacted both a tonne, e.g. Kalshi CTO came from the NEO scholars programme, and Cursor recently acquired another NEO portfolio company.

But almost none of that story has been told deliberately by NEO… The association between the fund and those outcomes is only really surfacing this week because a performance report scooped and circulated…. Probably not something other firms want to replicate.

The funds building durable brand advantage are the ones closing that gap on purpose - before the scoop, before the rumour, before someone else tells the story.

Laurie, Refinery Media

If you made it all the way through, thanks so much for reading! Several hundred VCs now open this every week. If it's helped you think differently about marketing, Venture, or storytelling, please send it to someone in your orbit.

If you enjoyed this, read more from our top posts: